It is essential for businesses to understand how their assets can lose value, especially when it comes to financial reporting and planning. If you’ve ever wondered what depreciation is and why it matters, you’re not alone.

Depreciation plays a key role in accounting by spreading the costs of your assets over a longer period of time, helping to reflect their true value.

In this guide, we’ll break down what depreciation is, how it is calculated, and the different methods businesses use to apply it.

What is depreciation?

Depreciation is a method in accounting that’s used to spread the cost of a tangible asset over its useful life. So, instead of recording the full expense when you buy an asset, depreciation will spread that cost gradually over time (typically over the asset’s expected useful life).

It’s an accounting method commonly used for assets like vehicles and machinery, as these items generally lose their value – for example they can be worn down over time or made obsolete by newer models.

It’s important to note that depreciation is a non-cash expense. Although cash was spent when the asset was purchased, depreciation will reflect the gradual reduction in value over several years, impacting financial statements by lowering the overall reported profit and the asset’s book value.

How do you calculate depreciation?

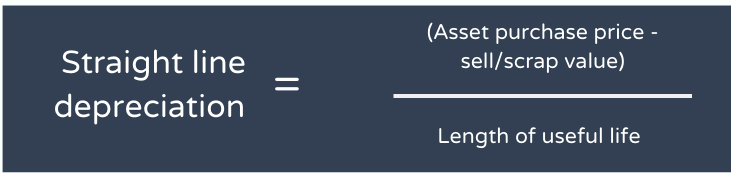

Depreciation is calculated using the following formula:

Depreciation = (Cost of Asset – Salvage Value) / Useful Length of Life

Here’s a rundown of each part:

- Cost of Asset: The total amount paid to purchase the asset and prepare it for use. This can include delivery, installation, and setup costs.

- Salvage Value (Residual Value): The estimated value of the asset at the end of its useful life.

- Useful Life: The period of time the asset is expected to generate value for the business, usually valued in years.

Example of depreciation calculation

Imagine a company buys a vehicle for £50,000. It expects the vehicle to be worth £5,000 at the end of five years.

- Depreciation = (£50,000 – £5,000) / 5 years

- Depreciation = £9,000 per year

The business would record £9,000 in annual depreciation expense for five years.

What is accumulated depreciation?

Accumulated depreciation is the total amount of depreciation recorded for an asset since it was purchased.

On the balance sheet, accumulated depreciation appears as a contra-asset account, meaning it reduces the asset’s original cost to show its net book value.

For example:

- Asset cost: £50,000

- Accumulated depreciation: £18,000

- Net book value: £32,000

Tracking the accumulated depreciation of an asset helps businesses understand its remaining value and calculate the gains or losses if the asset is sold.

What kind of assets can you depreciate?

Tangible fixed assets can be depreciated. These include:

- Buildings

- Machinery

- Equipment

- Vehicles

- Furniture

Intangible assets such as patents and copyrights are usually amortized rather than depreciated, though both methods involve spreading the cost over a period of time.

Types of depreciation

Different assets lose value in different ways. That’s why several depreciation methods exist. The right choice depends on the asset and your accounting policies.

1. Straight-line depreciation

Straight-line depreciation is the simplest and most widely used method.

It spreads the asset’s cost evenly across its useful life. Each year, the same depreciation amount is recorded.

This method works well for assets that provide consistent value over time.

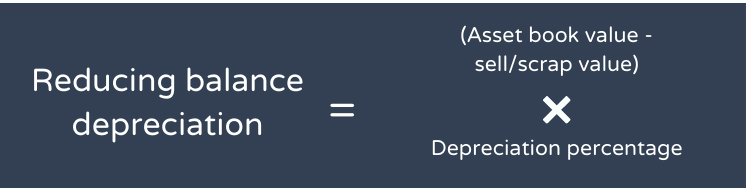

2. Declining balance depreciation

The declining balance method (also called reducing balance or accelerated depreciation) records higher depreciation expenses in the early years and smaller amounts in later years.

This approach assumes the asset is more productive or loses value more quickly in its early life. It can be used for technology, vehicles, and equipment that becomes obsolete faster than other types of assets might.

3. Sum-of-the-Years’ Digits (SYD)

The Sum-of-the-Years’ Digits (SYD) method is another type of accelerated depreciation.

It calculates depreciation using a fraction based on the asset’s remaining life.

For example, if an asset has a five-year life:

1 + 2 + 3 + 4 + 5 = 15

That total (15) becomes the denominator in the depreciation formula. The depreciation expense decreases each year as the remaining life shortens.

SYD is commonly used when assets lose value more rapidly at the beginning of their life.

4. Units of production depreciation

Unlike time-based methods, units of production depreciation is based on actual usage.

Instead of calculating depreciation by year, it’s calculated according to:

- Units produced, or

- Hours used

This method is often used in industries that own manufacturing machinery or equipment, where the wear of the product depends on output rather than time.

5. Modified Accelerated Cost Recovery System (MACRS)

The Modified Accelerated Cost Recovery System (MACRS) is the U.S. tax depreciation system introduced by the Tax Reform Act of 1986.

Under MACRS:

- Assets are assigned to specific classes

- Each class has a defined recovery period (ranging from 3 to 39 years)

- Accelerated methods such as double-declining balance are commonly used

MACRS allows businesses to recover asset costs more quickly for tax purposes, reducing taxable income in the earlier years of their lifecycles.

What is a depreciation schedule?

A depreciation schedule is a detailed record that shows how an asset’s value has decreased over time.

It typically includes:

- Asset cost

- Overall salvage value

- Useful life period

- Depreciation method

- Annual depreciation amounts

- Accumulated depreciation

- Net book value

Depreciation schedules are essential for financial reporting, tax planning, budgeting, and long-term forecasting.

Comparing depreciation methods

Choosing the right depreciation method depends on:

- The type of asset

- How the asset is used

- Financial reporting goals

- Tax considerations

Straight-line offers simplicity and consistency. Accelerated methods provide higher early deductions. Usage-based methods offer precision for production-heavy assets.

The best method is the one that most accurately reflects how the asset generates value for your business. It will often be industry dependent.

Depreciation and Brixx Software

Tracking assets and maintaining accurate depreciation schedules can become complex as a business grows. It can be difficult to manage these in a spreadsheet tool like Excel.

Financial modelling tools like Brixx help businesses:

- Track fixed assets

- Automate depreciation calculations

- Generate financial reports

- Improve forecasting accuracy

Instead of relying on manual spreadsheets, financial forecasting tools can simplify depreciation management and support better financial planning.

Commonly asked questions

How do you find the rate of depreciation?

To calculate the rate of depreciation, you first need to understand a few key figures about the asset: its original cost, its estimated salvage value, and its useful life.

Here’s how it works step by step:

1. Identify the initial value of the asset

This is the purchase price, including any costs required to get the asset ready for use.

2. Estimate the salvage value

The salvage value (also called residual value) is the estimated amount the asset will be worth at the end of its useful life. This figure is typically based on industry standards or a professional estimate.

3. Determine the useful life

Useful life refers to how long the asset is expected to provide an actual economic benefit to the business. It’s usually measured in years and based on past experience or industry guidance.

4. Calculate annual depreciation expense

Use this formula:

Depreciation Expense = (Initial Value – Salvage Value) ÷ Useful Life

5. Calculate the depreciation rate

To express depreciation as a percentage:

Rate of Depreciation = (Depreciation Expense ÷ Initial Value) × 100

Example

If an asset costs £10,000, has a salvage value of £2,000, and a useful life of 5 years:

Annual depreciation = (£10,000 – £2,000) ÷ 5 = £1,600

Depreciation rate = (£1,600 ÷ £10,000) × 100 = 16%

So, the asset depreciates at a rate of 16% per year under the straight-line method.

Why are assets depreciated over time?

Assets are depreciated because they gradually lose value. This decline can happen for several reasons, including physical wear and tear, regular usage, aging, or technological obsolescence.

In accounting, depreciation provides a structured way to spread the cost of a long-term asset across the period it generates revenue. Rather than recording the full cost upfront, businesses allocate the expense over the asset’s useful life, for example over 5 years.

This approach supports the matching principle in accounting (which aligns expenses with the income they help produce) and ensures financial reports present a more accurate picture of profitability and asset value.

How are assets depreciated for tax purposes?

For tax reporting in the United States, depreciation follows rules set by the Internal Revenue Service (IRS).

The most commonly used system is the Modified Accelerated Cost Recovery System (MACRS), which we have previously covered.

This system enables businesses to recover the cost of qualifying assets over a fixed schedule, reducing taxable income according to federal tax guidelines.

Is depreciation considered to be an expense?

Yes, depreciation is considered an expense in accounting.

More specifically, it’s a non-cash operating expense that reflects the gradual reduction in an asset’s value over time. Although no cash leaves the business when depreciation is recorded, it reduces reported profit on the income statement and lowers the asset’s book value on the balance sheet.

Depreciation helps businesses measure the true cost of using long-term assets and maintain accurate financial reporting.