Before we dive into a profit and loss example, the profit and loss report, love it or hate it, it’s an essential tool for understanding the performance of your business.

If you’re not familiar with a P&L statement the terminology can be confusing. For instance, what’s the difference between gross profit and net profit? What should be included in cost of goods sold vs operating costs?

To clear this all up, I’m going to use an example coffee shop business to show where all the elements sit in a typical profit and loss. I’ve broken it down section by section so you can see where everything belongs from sandwich sales to the purchase of coffee beans. The example Profit & Loss below was built in Brixx, however you can also make it in our free profit & loss spreadsheet template too.

Profit and Loss Example

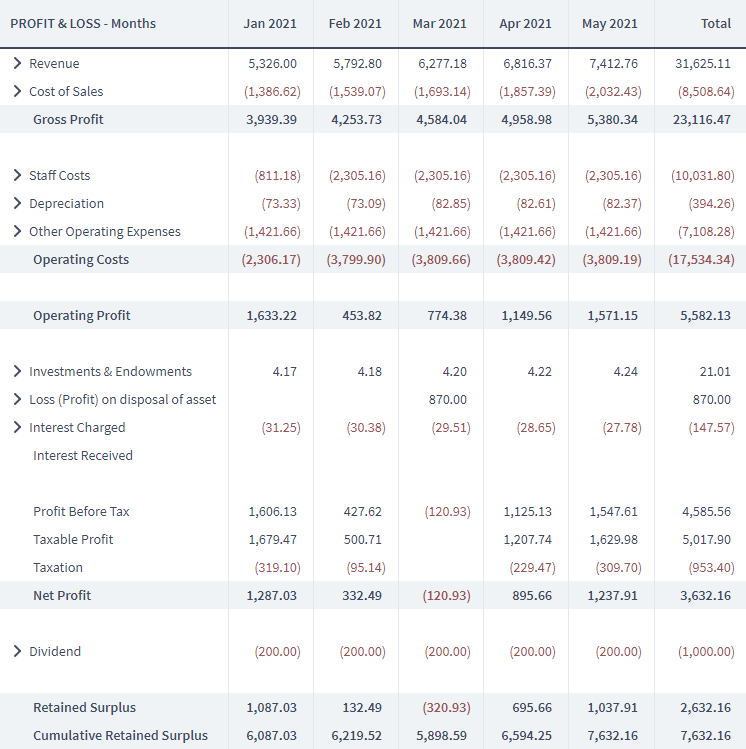

The table below is my profit and loss example’s coffee shop’s P&L Report which displays my business’ profits and losses each month.

We’re going to cover this in three parts:

- Gross Profit

- Operating Profit

- Net Profit

What goes into gross profit?

Gross profit is the money a company makes after all costs related to making and selling its products have been deducted.

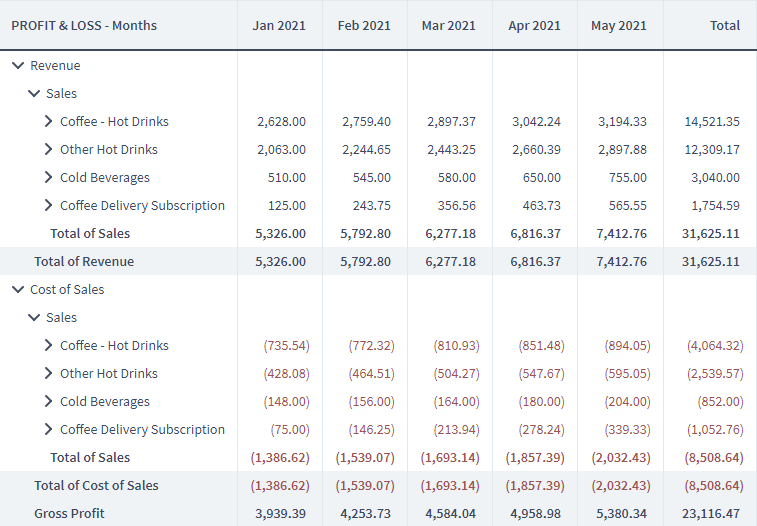

Gross profit is made up of two sections – revenue and cost of sales.

- Revenue – Revenue from a transaction appears on the P&L the day it was earned or invoiced, even if the cash hasn’t been received from this transaction yet. This sets apart the P&L and the cash flow statement, as in the cash flow, cash is noted when the company actually receives it. For example, my coffee shop gets revenue from selling coffee, tea and cakes.

- Cost of sales – “Cost of goods sold” are costs directly related to the creation and delivery of a product or service. This could be manufacturing, inventory purchases or delivery fees. In my coffee shop business, some of my cost of sales are coffee beans, milk and take-away cups.

What goes into operating profit?

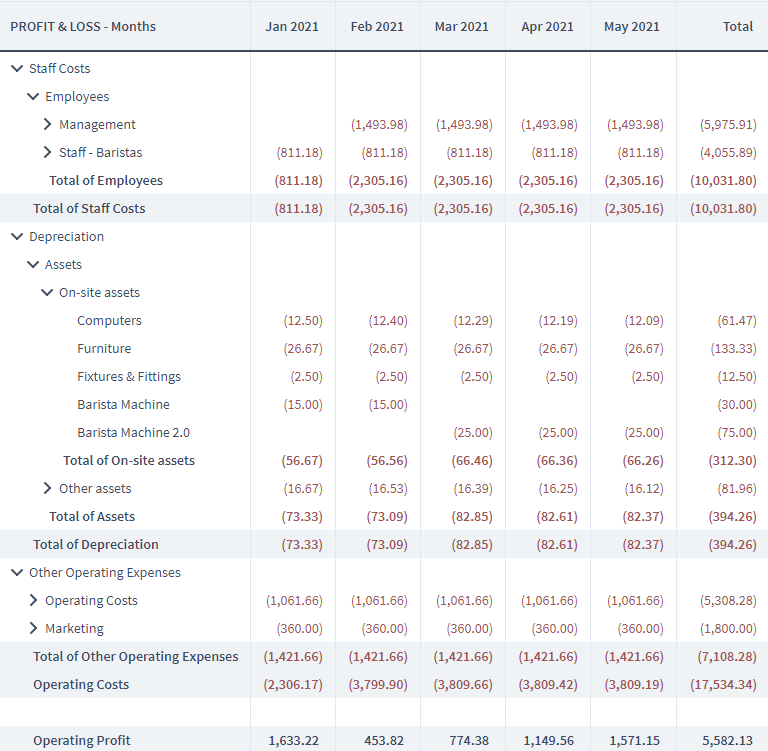

Operating profit is calculated by totalling up your operating expenses and deducting them from gross profit.

Operating costs are all the costs associated with the day-to-day life of your business. These include the costs of paying staff, insurance and utility bills such as power and water etc.

These costs do not include costs of sales which were included in gross profit above…

Staff costs – Staff costs include the salaries of the people a company hires, as well as associated costs such as National Insurance and pension payments. In my coffee shop example, I have three employees – a general manager and two baristas.

- Depreciation – Assets your business owns lose value over time due to wear and tear. This type of loss is called depreciation. My coffee machines are worth a lot of money, but this value drops over time as they get used.

- Other operating expenses – The rest of your business running costs sit here. For my coffee shop business, we’ve got costs like rent, insurance, utility bills, maintenance etc.

What goes into net profit?

Net profit is calculated by totalling up any other activities such as tax, investments and interest and then deducting them from operating profit.

- Investments and endowments – This is where a company invests its money either into external activities or into another company.

- Loss (profit) on disposal of asset – Loss on disposal of an asset shows when you get rid of an asset, either by writing it off or by selling it. If an asset is sold for less than its value, a loss would be shown here, while a profit would be shown if an asset was sold for more than its value. In my example, in March I had to buy a new coffee machine. As I disposed of the old machine, its value of £870 is shown as a loss to my business.

- Interest charged – This is the amount of money you pay as interest on top of any money you’ve been loaned.

- Interest received – This is money earned from savings kept in bank accounts. My coffee shop’s savings receive 1.5% interest per annum.

- Profit before tax – Profit Before Tax is the total of everything in the profit & loss statement up to this point. It includes all of the lines above it, even if they aren’t taxable.

- Taxable profit – This shows profit before tax, but only includes lines which can be taxed. Lines like depreciation are excluded. The depreciation losses from my assets, including the coffee machine and furnishings, are not counted towards taxable profit.

- Taxation – Taxation shows how much money is owed to the government through corporation tax. So, out of my taxable profits, I pay 19% to the government.

- Net profit – Net Profit is the total profit (or loss) after all costs and tax have been deducted from revenue sources.

- Dividends – A dividend is money which a company pays to its shareholders. As the owner of the coffee shop, I invested a sum of money to start my business, and in return, I receive a percentage of its profits in the form of a dividend.

- Retained surplus – To work out retained surplus (your total profit or loss for that month), subtract your dividend costs from your net profit. Unfortunately, in my first month of business (Jan 2018) I made a loss. However, in the cumulative retained surplus section, I still have retained profit. This is because it takes into consideration profits retained from the business’ previous operations.

Going through the P&L line-by-line is a great way to understand how your revenue flows through the business, and how different costs affect your profit.

So why is it so important to forecast your P&L?

Why should you forecast your profit and loss sheet?

A profit and loss forecast is something which every business can benefit from. It allows for your income and expenses to be accounted for from the moment you receive them, even if cash hasn’t passed hands.

- A profit and loss forecast includes several key performance indicators that show how the business may perform. It is the basis of all financial profitability ratios, which can be used to assess the efficiency of the business’ operations.

- Planning your expected revenue is an important part of profit and loss forecasting. While many say that ‘cash is king’, it can also be volatile and hard to predict. Planning revenue gives you an idea of the sales your business will be making, and the continued value the business will need to give to its customers.

- Most importantly, the profit and loss shows the extent of your profits or losses if you take the course of action you have forecast. This gives you the confidence to move ahead more cautiously in times where profit is low, and grow rapidly when periods of high profit are likely. Understanding how much and when the business is profitable helps you to gauge the risks the business can take, in terms of further investment in people and resources.

Conclusion

We’ve now covered the P&L line by line. You should now understand that as you work down the report, you gradually add and deduct gains and losses to the business.

Think of the P&L like a waterfall. This waterfall effect shows how revenue is used by different areas of the business, finally trickling down to a final profit figure for the period once all expenses and other modifications such as asset sales have been taken off.

In isolation, each section is quite easy to understand. How they link to one another to complete the statement can be tricky to get your head around. Hopefully, by breaking down each section, you now know how each part links into one another.