What is a cash conversion cycle (CCC)?

The Cash Conversion Cycle (CCC) is a crucial financial metric used to evaluate the efficiency with which a business manages its inventory, receivables, and payables. It reflects the time taken to convert resources invested in inventory into cash flows from sales. A shorter CCC indicates a more efficient operation, highlighting quicker inventory turnover and faster collection of accounts receivable.

Recommended reading: How Do Payable Accounts and Receivable Accounts Interact with Cash Flow?

Get started with our forecasting software so that you can plan your business' future

Manage your cashflow with Brixx

What is the cash conversion cycle formula?

We have listed the Cash Conversion Cycle formula below:

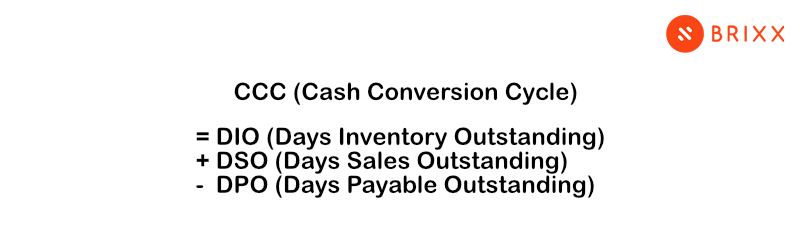

CCC = DIO + DSO – DPO.

This encompasses three key components:

- Days Inventory Outstanding (DIO)

- Days Sales Outstanding (DSO)

- Days Payables Outstanding (DPO)

Each component plays a vital role in measuring different aspects of a company’s cash flow process. The CCC formula effectively combines these elements to provide a comprehensive view of how efficiently a company is managing its cash conversion cycle.

How to calculate your cash conversion cycle?

1. Calculate days inventory outstanding (DIO)

Days Inventory Outstanding (DIO) measures the average time a company holds inventory before selling it. The formula to calculate DIO is:

DIO = (Average Inventory / Cost of Goods Sold) * 365.

This number will indicate how well a company manages its inventory.

2. Calculate days sales outstanding (DSO)

Days Sales Outstanding (DSO) reflects the average number of days it takes for a company to collect payments after sales. DSO is calculated using the formula:

DSO = (Average Accounts Receivable / Total Credit Sales) * 365.

It shows the efficiency of the company’s credit and collections process.

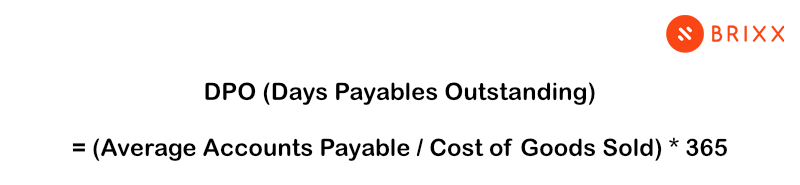

3. Calculate days payables outstanding (DPO)

Days Payables Outstanding (DPO) indicates the average time a company takes to pay its invoices. The formula for DPO is:

DPO = (Average Accounts Payable / Cost of Goods Sold) * 365.

This metric sheds light on the company’s payment strategy to its suppliers.

4. Calculate CCC

Finally, to determine the CCC, simply use the formula:

CCC = DIO + DSO – DPO.

This calculation provides a comprehensive view of the time taken by a company to turn its inventory investments into cash through sales.

Example of the cash conversion cycle

We will have a look at an example to illustrate the Cash Conversion Cycle (CCC). Assume a company has an average inventory of $50,000, cost of goods sold (COGS) of $300,000, average accounts receivable of $40,000, total credit sales of $500,000, and average accounts payable of $30,000.

- DIO = (Average Inventory / COGS) * 365 = ($50,000 / $300,000) * 365 = 60.83 days

- DSO = (Average Accounts Receivable / Total Credit Sales) * 365 = ($40,000 / $500,000) * 365 = 29.2 days

- DPO = (Average Accounts Payable / COGS) * 365 = ($30,000 / $300,000) * 365 = 36.5 days

- CCC = DIO + DSO – DPO = 60.83 + 29.2 – 36.5 = 53.53 days

This example indicates that it takes the company approximately 53.53 days to convert its investments in inventory and resources into cash flow from sales.

Why calculate cash conversion cycle?

Calculating the CCC is critical for businesses to understand their efficiency in managing working capital. It provides insights into how quickly a company can convert its inventory into sales and then into cash. A shorter CCC indicates a healthy cash flow, enabling a business to pay debts, reinvest in operations, and reduce reliance on external financing. It also helps in identifying areas for improvement in inventory management, credit policies, and payment terms with suppliers.

What is a good cash conversion cycle?

A “good” CCC varies by industry and business model. Generally, a shorter CCC is preferable as it indicates a faster conversion of inventory and receivables into cash, which is vital for maintaining liquidity and funding ongoing operations. However, it’s important to benchmark against industry standards and historical performance to determine what is optimal for a specific company. For some businesses, a longer CCC might be normal due to the nature of their operations or industry practices.

What is negative cash conversion cycle?

A negative Cash Conversion Cycle (CCC) occurs when a company’s Days Payables Outstanding (DPO) is greater than the sum of its Days Inventory Outstanding (DIO) and Days Sales Outstanding (DSO). This situation means that the company is able to pay its suppliers after it has already sold its inventory and collected the receivables. In essence, the company is using the suppliers’ funds to finance its operations, which can be a sign of efficient cash management. This allows the business to hold onto cash for other uses, such as investment or debt reduction, without impacting its working capital.

How to shorten your cash conversion cycle

Shortening the Cash Conversion Cycle (CCC) is crucial for improving a company’s liquidity and operational efficiency. Here are some strategies to achieve this:

- Optimize inventory management: Reduce DIO by implementing just-in-time (JIT) inventory systems, improving demand forecasting, and eliminating obsolete stock. Efficient inventory management means less money tied up in unsold goods

- Enhance credit management: To lower DSO, tighten credit terms, conduct credit checks on new customers, and implement effective collections procedures. Offering early payment discounts can also encourage faster customer payments

- Extend payment terms with suppliers: Negotiating longer payment terms with suppliers can increase DPO, allowing your business to use the cash on hand for longer periods without affecting supplier relationships

- Leverage technology: Utilize financial management software to track and analyze CCC components more effectively. Automated systems can help in promptly identifying bottlenecks and opportunities for improvement

- Review and adjust pricing strategies: Ensure that your pricing strategy not only covers costs but also provides sufficient margins to maintain healthy cash flow

- Regular review of financial metrics: Continuously monitor financial metrics and the CCC to spot trends, identify issues early, and make timely adjustments

We can help

At Brixx, we offer targeted tools to help optimize your Cash Conversion Cycle and enhance your financial management:

- Cash flow forecasts: Our software provides detailed 10-year forecasts for cash in and out, critical for managing your Cash Conversion Cycle effectively

- Automated accounting: Generate essential financial reports like Profit & Loss, and Cash Flow statements automatically, ensuring up-to-date and accurate financial tracking

- Scenario testing: Experiment with ‘what-if’ scenarios to understand how changes in your operations can impact your Cash Conversion Cycle, allowing for strategic decision-making

Explore how Brixx can transform your financial management and optimize your Cash Conversion Cycle.